kathyc2

-

Posts

497 -

Joined

-

Last visited

-

Days Won

26

Everything posted by kathyc2

-

It sounds like this would be overcomplicating things. Why do you/they want two different companies? Do they share the same building? Is food purchased, and then the same sold or used in luncheonette? Do you or they really want to do all the accounting to allocate between the business cost of food, rent, utilities, insurance, etc? Why not keep it cleaner and have one LLC that opts to be taxed as a S corp?

-

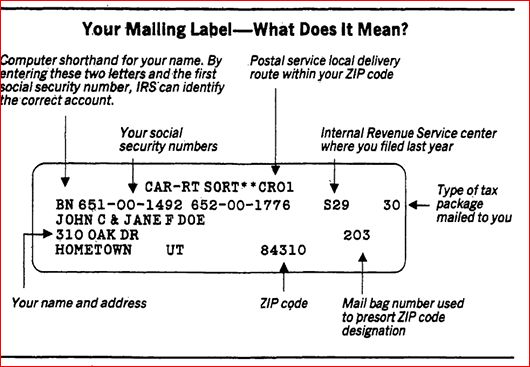

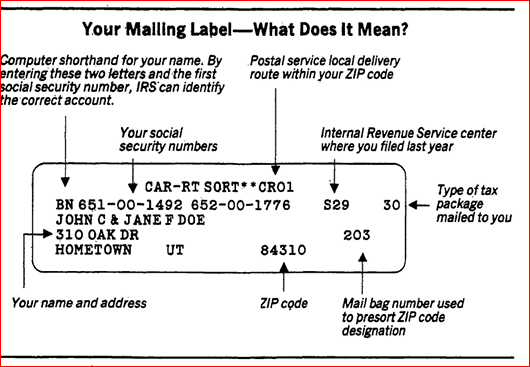

Anyone else remember when IRS sent mail with a label with SSN clearly visible? How times have changed!

-

I need slight (.75) magnification for paper/computer work. However, then things are blurry in distance. I solved it by ordering glasses with left lens plain glass and right side with magnification. Much easier to deal with than bifocals.

-

Why can't they get an ACA plan? Unless over age 65 or coverage available, which doesn't seem to apply, they can buy insurance there. Of course they wouldn't get premium assistance, but they would have coverage. Plans may not be the greatest, but they can't be denied due to health problems. As pointed out, a charitable donation from a Sch C or S corp would not lower MAGI.

-

It used to be my goto source to answer questions. I find it much easier to google what I want rather than open index of a book and then turn to the page where it's addressed. I think a lot of hard copy reference material has gone the way of a paper phone book.

-

I'm confused on how they are making 300K, can live on 40K, yet can't afford insurance????

-

It's kind of a touchy situation. If someone is truly abused, I wouldn't want to give the impression that I don't believe them. On the other hand, they may just be claiming it to save money. Use your gut instinct, but I think I would have the TP write out and sign a description to keep in file and explaining to them that you need this for both of your protection.

-

I've not had that but it stinks that we need to act as social workers to prepare a tax return. Is the spouse that is claiming abuse the only one that had ACA? Had you prepared prior returns for them?

-

If one of the spouses qualifies as HOH you don't need to worry about the domestic abuse exception. I would just use the normal due diligence for HOH.

-

I'm confused as to what your goal is. Is it to raise fees with the goal of doing less returns and still having the same revenue? Is it certain types of returns you no longer want to prepare?

-

Are you using the living apart and qualifying as HOH exception? Or, the domestic abuse exception?

-

My understanding is the "changes" were meant to be temporary. I suppose there is a small chance that some are extended in lame duck session, but after we have divided gov't with the new Congress in January I highly doubt they will be extended.

-

I learned a long time ago that tax policy will never be fair, as "fair" is a subjective term.

-

The 65 restriction does NOT apply if there are qualifying children.

-

Because I'm set in my ways! It took me at least 2 years to get used to where things were on the "postcard" return while reviewing. Now it's hide and seek again where they moved things.

-

I've used office supply places like Staples and also Amazon. I order by part rather than set as I don't need 5 copies of 1099.

-

What the heck are they doing? Many, many lines added to "main" forms with obscure stuff I've never encountered in 25 years. Not just on the 1040 but also Schedules 1, 2 and 3. Uggghhhh! https://www.irs.gov/pub/irs-dft/f1040--dft.pdf

-

I think the unlimited subscription has the best bang for the buck. Most you can do self study, webinar, etc. A word of caution. Some have in small print that they will auto renew the next year. You need to set a reminder on your calendar to cancel that before it happens.

-

The 19,560 only pertains to income subject to FICA tax, not investment income. The 19,560 is also per person, not tax return. If a 15 wage/ 10 investment return split is reasonable is another matter.

-

2022 SLCSP Lookup - healthcare.gov only has 2021

kathyc2 replied to BulldogTom's topic in General Chat

There's a couple different ways to approach it. If you are putting in their financial data, it will calculate the credit based on SLCSP. If they went through healthcare.gov rather than an agent, they can log in to their account and find out a lot of info. Under messages there will be a message about marketplace eligibility. This will tell them the income they used to apply and the amount of credit they will receive based on that income. Since you say they want to know how much they will need to pay back, I assume their income is higher than what they used to apply. Put in the higher income keeping ages, and people that same as when they applied to see what the credit would be at that level. if the 795 credit is calculated on the new projected income, just take the difference between that credit and the credit when they applied to see the payback. If they are under 400% FPL the payback may be limited. If you don't know what the original credit is they received, then you need to go about it a little differently. You will need to know the exact plan they chose and then calculate the difference between the full price plan and the amount they are paying. That will give you the calculated credit when they applied. This probably isn't clear, so let me know which part needs further clarification. -

2022 SLCSP Lookup - healthcare.gov only has 2021

kathyc2 replied to BulldogTom's topic in General Chat

Here is the link: https://www.healthcare.gov/see-plans/#/ You need to be a little careful as SLCSP is not always obvious. They only use the core medical to determine it, so plans that have dental or vision can skew the numbers. -

https://apnews.com/article/biden-misinformation-health-care-reform-internal-revenue-service-fb835c1099dad4cca5ff893bfd07d466 Included in article: "He added that members who are of retirement age have expressed a greater desire to retire due to the increased attention on their jobs. More than half of the IRS’ enforcement workforce of 80,000 is retirement eligible."

-

I would prepare the 5329 and request the waiver. You don't need a note from the Dr. Just indicate that it was an oversight and that both the 2021 and 2022 have been removed from the account. I've had several of these over the years and never once did they access the penalty.

-

how do you track tax returns thru the in and out cycle of the office

kathyc2 replied to schirallicpa's topic in General Chat

Lots of different ideas and suggestions. Everyone needs to determine what works best for THEM. -

IRA Act - get ready for Energy Credits Confusion

kathyc2 replied to BulldogTom's topic in General Chat

Probably good advice from a tax perspective due to the limits on payback based on % of FPL. Insured are told to contact the marketplace if income changes, so be careful of ethics if recommending to wait.