G2R

-

Posts

227 -

Joined

-

Last visited

-

Days Won

3

Everything posted by G2R

-

Was reading an article from Kiplinger regarding expanded cases when on Schedule E, Page 2, Line 28, the box labeled "check if basis comp required" is checked. I'm about to file my only S Corp return this year that has a loss to report and I can't see how ATX even utilizes this box unless I override. Even in the K-1 Detail Anyone ever check this box without an override and if so, how? And while we're discussing it, how many are actually doing the basis computation and including it with the return when their reporting a loss? I've spoken to other accountants who looked at me like I had three heads when I mentioned it.

-

You honestly, genuinely and sincerely just made my day

-

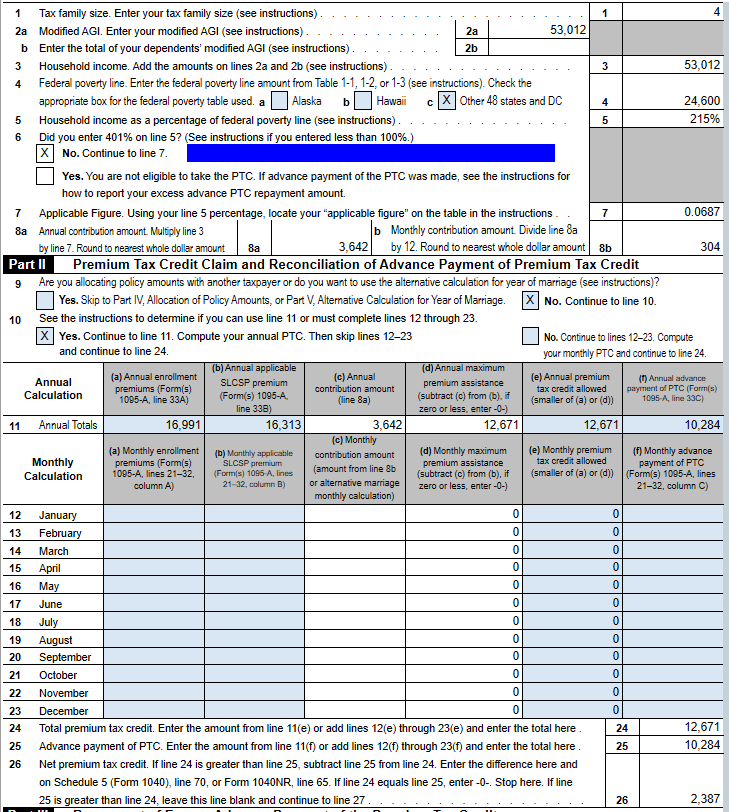

Resurrecting this beast as I'm really trying hard to do this RIGHT, and it genuinely feels impossible using the 974 as a guide. I'd honestly LOVE to see an IRS auditor explain this whole thing. I'd bet many can't. Regardless I've got a CRAZY method and I'm hoping one of you can logically talk me out of it. I'm using ATX. I've already completed the SE Health Ins. worksheet, Worksheet W & Worksheet X and form 8962. The only thing blank on W is the very bottom where it asks for the simplified or iterative method results. THEN, I took total premiums listed on 1095A (ie $16k) minus premium tax credit listed on 8962, line 24 ($13k) = $3k. So I then reduce my SE Health insurance deduction by $3k. Let's assume I was deducting $7k in premiums originally, so now it only says $4k. I go back to 8962, see what the newly calculated premium tax credit says and continue to adjust the SE Health insurance number up and/or down until I get a summation of SE Health insurance and Premium tax credit that's most closely totals the total premiums. Is this crazy? Is this in effect the Iterative calculation?

-

Resurrecting this beast as I'm really trying hard to do this RIGHT, and it genuinely feels impossible using the 974 as a guide. I'd honestly LOVE to see an IRS auditor explain this whole thing. I'd bet many can't. Regardless I've got a CRAZY method and I'm hoping one of you can logically talk me out of it. I'm using ATX. I've already completed the SE Health Ins. worksheet, Worksheet W & Worksheet X and form 8962. The only thing blank on W is the very bottom where it asks for the simplified or iterative method results. THEN, I took total premiums listed on 1095A (ie $16k) minus premium tax credit listed on 8962, line 24 ($13k) = $3k. So I then reduce my SE Health insurance deduction by $3k. Let's assume I was deducting $7k in premiums originally, so now it only says $4k. I go back to 8962, see what the newly calculated premium tax credit says and continue to adjust the SE Health insurance number up and/or down until I get a summation of SE Health insurance and Premium tax credit that's most closely totals the total premiums. Is this crazy? Is this in effect the Iterative calculation?

-

Ugh, I did a search in the forum for this before I posted and came up dry. Guess my searching skill need work. Thansk Pacun.

-

And I found it. Never mind. For anyone looking, it's under the "over 65, blind, deaf, etc." boxes.

-

Rolled over a client's return from last year where his mother claimed his exemption. His mother cannot claim him this year, but the box at the top for "Someone can be claimed as a dependent" is checked and for the love of me, I cannot find out how to remove this. HELP!

-

This is what I thought too, however, after researching it and I think because it doesn't qualify as a 2nd home (they didn't stay in it the minimum of 15 days necessary to qualify as a 2nd home), then that rule doesn't apply. https://www.redweek.com/resources/articles/tax-aspects-renting-timeshare

-

Client owns a 3 week timeshare. Uses it for 11 days personally, rents it out for 10 days. Got a 1099 for the rental income. Just want to confirm. The timeshare doesn't qualify as a 2nd home because they didn't personally use it for 15 days correct? I report it on Sch E, but losses are limited to rental income. After that they are disallowed, correct? Do I have to split the association fees and other expenses between personal and rental? Meaning, only (10/21 or 48%) of expenses are deductible on Sch E? Are the disallowed losses carried forward or permanently disallowed?

-

Did you complete this line?

-

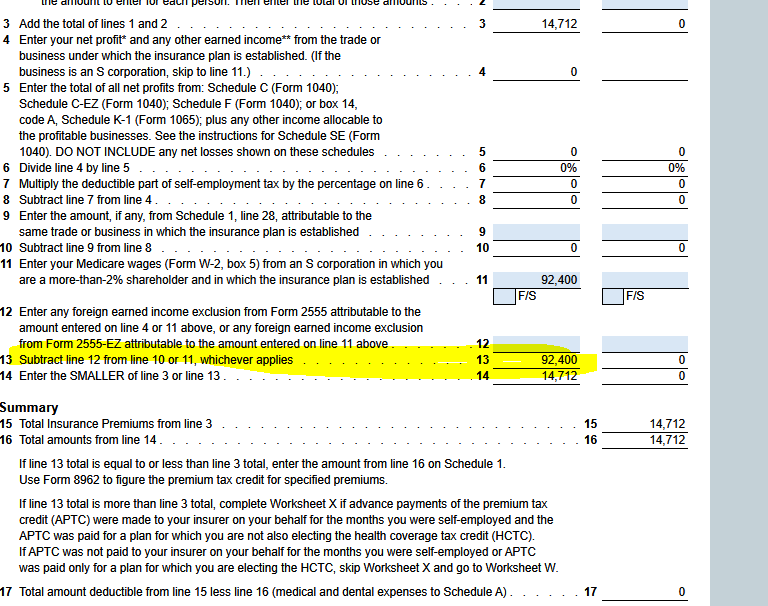

This data entry is very tricky indeed. I always have to pull away the cobwebs from last year to remember how I did it before. After I've enter everything I think should be enough, the business name never shows up in the "choose the business under which the plan is established" list. Then, on the K-1 schedule data entry, in the DETAIL tab, Box 12, letter S, "amounts paid for medical insurance," when I enter the SE health insurance amount again here, this seems to illuminate the business name in the Line 29, Sch 1 worksheet of the 1040.

-

I didn't even know about this feature. Been doing it the old fashion pen-and-paper way! Thanks for the tip!

-

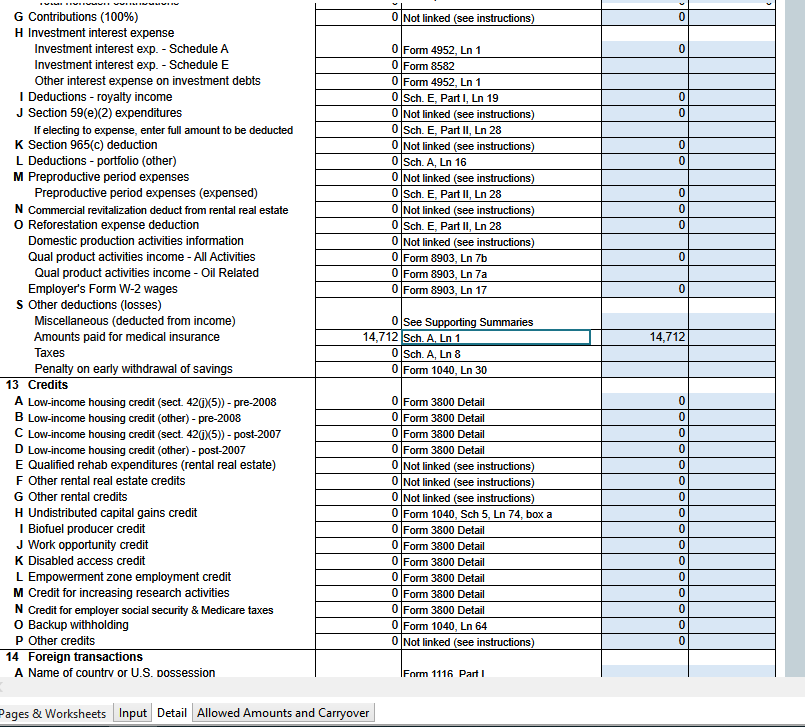

On the 1120S page, click on the pages & worksheets tab on the bottom, jump to the line 17d page worksheet, scroll to the bottom and start with line "V."

-

I'm stunned by the number of NEW clients I get that were incorporated by other lawyers, accountants, etc and did not have the articles of incorp, by laws, minutes, or stock certificates issued. None of this was completed. Some clients have no idea where the corporate book is? Some were just given articles of incorp and blank by laws, minutes, stock certificates and did not provide guidance or insistence that this be completed BEFORE the company opened (let alone before the first tax return was filed.) So my question is. Do you request to see the corporate (black) book when interviewing a new corporate client? Do you verify the corporate details against what's on past corporate returns filed by another accountant? When, or if, you incorporate a client, do you just send them off to legal zoom or a lawyer and leave it up to them the corp in order? Do you ever check the book for accuracy? My terror on this subject comes from a story father (also an accountant) told me that happened years ago. New client comes in, says he's being audited. My dad reviews the bookkeeping and financials for him, requests to see the black book, but the client forgot it. On the day of the audit, the auditor requests to see the black book. New client says, "Oh, I've got that this time Bob!" Hands it to the auditor, (so my dad never got to review it) and low and behold, the lawyer screwed up the paperwork with incorrect dates and names, and worse, the stocks certificates were blank. The auditor denied the incorporation & S election based on the book being wrong. My dad said, the penalties and fees put the guy out of business. Has the IRS relaxed these rules over the years?

-

Interesting, I didn't know this. Thanks!

-

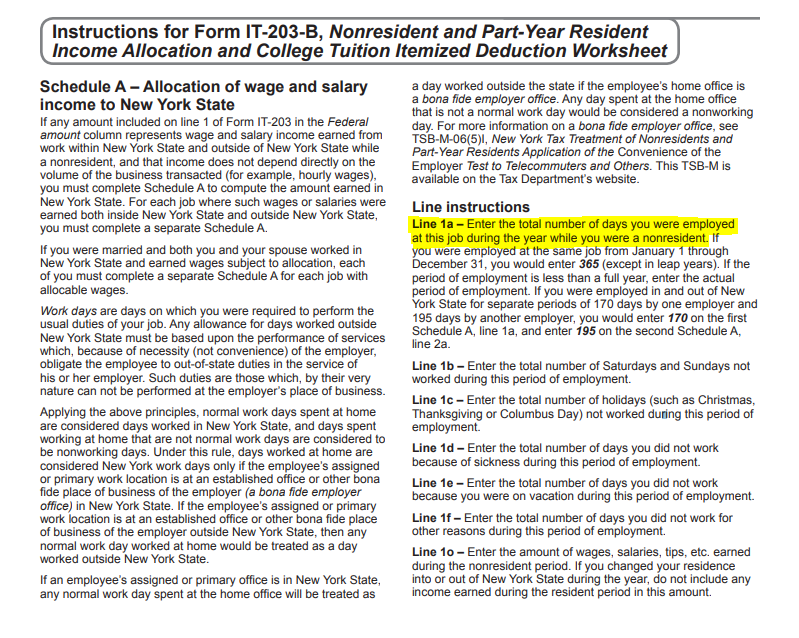

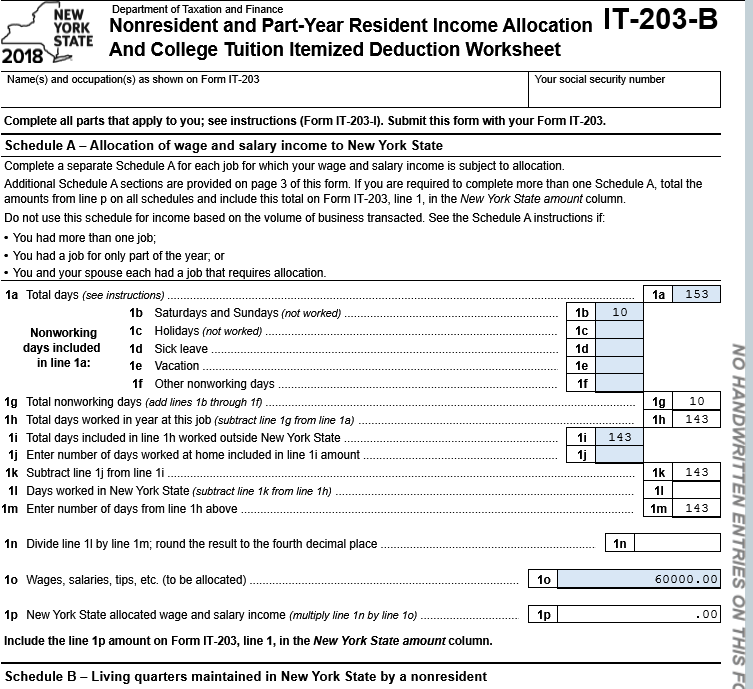

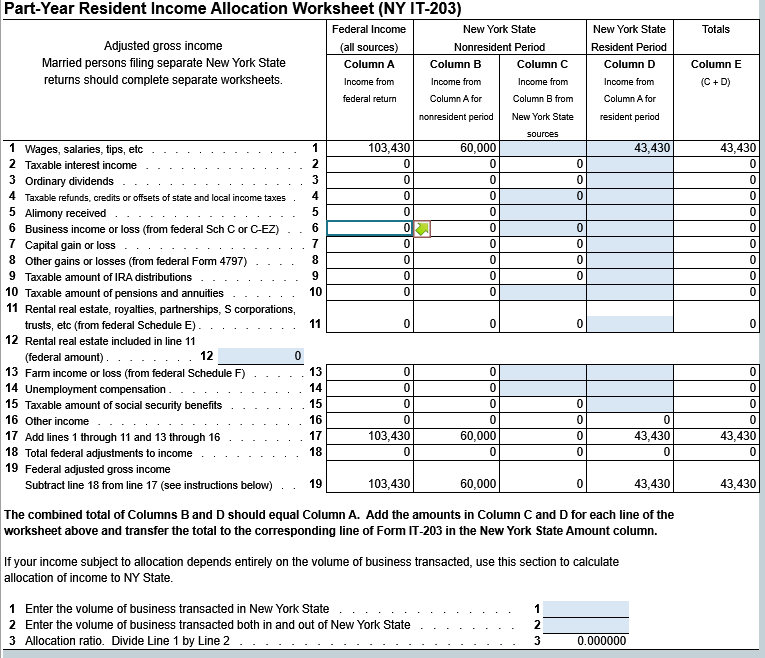

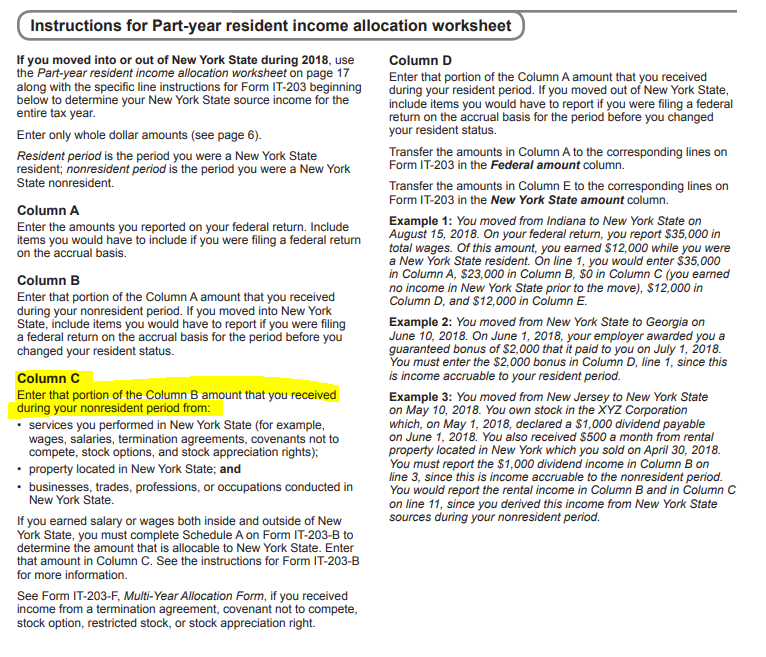

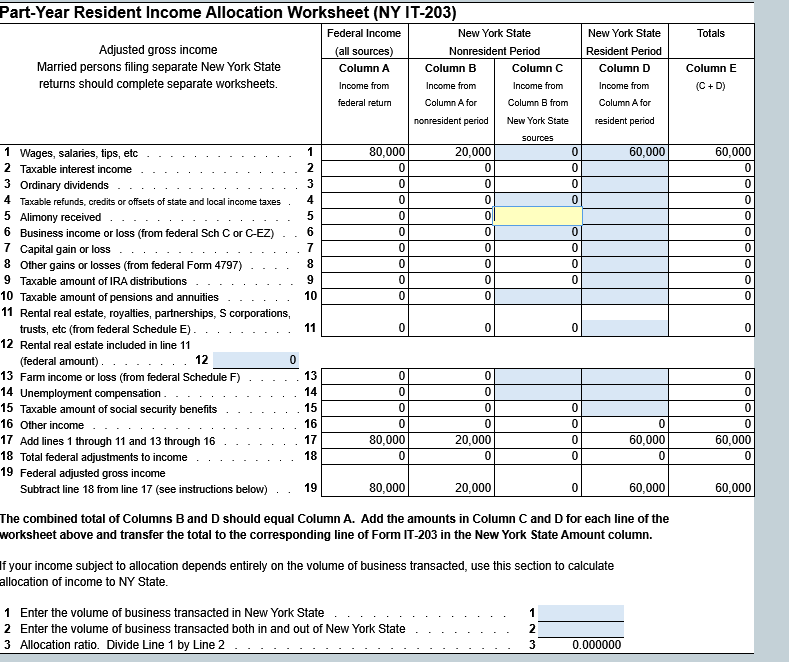

I think I see where you went astray. The instructions say for the IT-203B to enter NYS income info for when you were a nonresident of NY. You've entered the entire year and backed out the IL time. I think it should be entered like this (I'm just assuming $60k earned while in IL). You manually enter the IL wages on line 1o of the IT-203-B worksheet, then manually DELETE the Column C wages ATX flows to the Part-year Resident Income Worksheet for the NY IT-203

-

Does the W-2 at the bottom state the full wages as NYC wages? If so, ATX will automatically populate as fully earned in NYC. To correct this (which the employer should have listed only the wages they earned while working in NYC, and then started withholding IL wages going forward), you'll have to determine how much they earned during the time in NYC vs IL. Then on the NY IT203 worksheet, separate out what was the amount for the first months in NYC vs IL. Same is true for the other items listed on the worksheet. I usually have clients sum up the paychecks for the NYC months and the rest go to IL. If they didn't withhold IL taxes, he'll probably have a hefty bill for IL, but his NYS & NYC refund will likely cover this.

-

I believe so. Just remember to exclude 1/2 of the SE tax and any SE Health Insurance and SEP or Simple IRA contributions in your total. also, you might wait a couple days for the ATX update supposedly coming that might automatically flow this information for you so you have a double check on your numbers.

-

Just got done with ATX support. They said the latest ATX update will happen in 2 days and it will include the program automatically flowing the QBI info from the K-1 schedule into the 199A worksheet. Fingers crossed this is true.

-

I believe you have to reduce the QBI income only for simple IRAs because these retirement plans are put in place in direct connection with a small business. Same goes for SEP & Solo 401ks. Traditional and ROTH IRA contributions can be made by anyone, regardless of self employment status so that's why I don't believe these are part of the QBI equation. Many of the regulations use the term "effectively connected income" or "in relation to QBI" so the way I'm applying this is if it's related, connected or stemming from the qualified business income in some capacity, it's probably a factor in determining the QBI amount.

-

Assuming the SE Health Insurance & IRA contributions are NOT already included the $10k profit mentioned above, then you'd deduct them from the $10k profit, and you'd deduct 1/2 SE Tax which is calculated (10,000 x .9235) x .0765 = $706.48 So assuming SE Health Insurance was 2k, and IRA contributions were 1k. Then QBI would be as follows: QBI Calculation: Schedule C Profit $10,000, less $706.48 1/2 SE Tax less $2,000 SEHI less $1,000 IRA = $6.293.52 QBI So you get 20% of $6,293.52 assuming thresholds and/or SSTB isn't involved.

-

Just curious what everyone's client identity protection method is for remote clients. I'd say 95% of my clients I never see in person. They send all their tax backup, questionnaires, etc via email. I request all SS# be blacked out before sending. Then when I email them the tax return, e-file authorizations and bill, I use a OneDrive link with a 7-day expiration. But I'd love to hear other's methods and see if there's even more security I should do. Thoughts?

-

I agree with gfizer. Just file the amended. At least you caught it and can rectify relatively quickly.

-

Thank you Terry. ATX and I got to the same investment income number, but I had a slightly different "state, local & foreign income tax expense" number. (We're only off by $33 bucks so this isn't of real importance.) But I'm a ridiculous and just want to know how they got their amount. And all the "JUMP TO" links to give any insight into their calculation.

-

I hate ALL the new schedules. It's just a a waste of more paper!

I hate ALL the new schedules. It's just a a waste of more paper!