jklcpa

-

Posts

7,104 -

Joined

-

Days Won

396

Everything posted by jklcpa

-

Margaret is correct that client doesn't meet the eligibility test. He must use it 2 years out of the last five, 730 days. However, if a TP fails the eligibility test, it is still possible to take a partial exclusion IF certain other requirements are met. Those specifically allowed are: work-related move, health reasons, unforeseen circumstances, and other. You can find all of this general information in Pub 523 under the caption "Does Your Home Qualify for a Partial Exclusion of Gain? I don't think your client will qualify for the "unforeseen circumstances", but if you'd like to see the valid reasons IRS considers "unforeseen circumstances" you can read that in this older article from The Journal of Accountancy.

-

Back to your problem, maybe something changed in your system recently that is causing this. Do you know when the issue started? Maybe the topic below may help, and if you search the general chat forum for "freeze" "freezing" "crash" or "lockup" and sort by date, you will get more topics that may have something useful.

-

WK CCH doesn't care, and customer support has been awful ever since Glynn Willett sold the business. The reason this unofficial forum exists is because the company closed down the official forum on April 11, 2007 because some of the more outspoken users were complaining about the program, leaving users without any means of support or help. That is how little it cares about its customers.

-

From the perspective of the person buying something, paying a business expense, making a chartible donation, paying medical expenses, etc, the deduction is in the year that the charge occurs, as I've said for the 4th time now and with cites. This line of questioning reminds me of times when a non-tax pro sneaks through with a question and one of the reasons why we don't allow or answer questions from the general public on this forum. Also, one other post hidden that was off-topic.

-

Again, deduction is when the vendor, charity, medical provider, etc gets paid by the credit card company on behalf of the person who owes the money or is making a charitable contribution, etc. That person incurring the charge is using borrowed funds (on credit) to pay the bill. Like taking out a loan to pay the bill. Example: I purchase $15 of office supplies from Staples in Oct 2024 and charge that to my credit card, and it doesn't matter that I carry a balance on that credit card until after year end. I will deduct that expense in 2024 because Staples got paid in Oct 2024 by my credit card company on my behalf.

-

The deduction is taken in the year the payment to the payee occurs.

-

The purchaser has obligated him- or herself by paying the vendor with borrowed funds, so the deduction is when the charge occurs, not when the payment is made to the credit card company. Here are some references: Rev. Rul. 78-38 states that you may deduct a donation to a qualified charity via a charge to your bank credit card in the year the charge is made, regardless of when the bank is repaid Rev. Rul. 78-39 states the same rule for medical expenses. IRS Pub. 583, Starting a Business and Keeping Records (Rev. January 2007), p. 13, eludes to treatment of business expenses charged to a credit card using the transaction date for recording the deduction.

-

Yep, I know all about comebacks and warranty work. Husband is a now-retired mechanic, worked commission for most and then flat rate, and then worked as service manager too. On my end I've done the accounting and tax work for more than a few repair shops, quite a few gas stations, a couple of parts stores too, and a car dealer.

-

Just out of curiosity, are you trying to prepare a business return or Sch C using just the receipts, customer invoices, vendor invoices, and payroll records without having a complete set of books posted using double entry bookkeeping?

-

That is all correct.

-

You deduct whatever gross pay you pay the employees, no matter what job they are working on. It doesn't matter if it's warranty work or a first time repair.

-

I was just thinking about this today for when I eventually retire. If Drake is still offering PPR that includes some individual returns in the base price, that will be sufficient to prepare my return, siblings, and one or two friends.

-

Thank you! I haven't gone through all of my emails from this afternoon yet, but I do see it now.

-

IRS MeF operational status page: "Start-up for Business Returns will begin Wednesday, January 15, 2025, at 9:00 a.m. Eastern time." Date for individual returns: TBD

-

Annuity in an IRA - can surrender tax free if funds not leaving IRA

jklcpa replied to BulldogTom's topic in General Chat

Client should check the contract for its surrender period. Typically the penalty lessens as the date gets closer to the end of that period. ETA: no tax consequence if the reinvested funds stay within the IRA. -

If you are going to research this, the name is "Gillmore" and you may get more hits with the proper spelling. I have no personal experience with this, but found these interesting, for whatever they are worth: https://law.justia.com/cases/california/supreme-court/3d/29/418.html https://www.willicklawgroup.com/wp-content/uploads/2012/04/Gillmore-Gillmore-and-Trustee-Pay-over-Orders.pdf The second one is an older blog by an attorney that references the Dunkin case and that lays out different clauses that could have been employed but that Dunkin did not use that possibly could minimize tax impact, differences in tax brackets between the parties, and specific "tax intent" language. From reading all of this, it seems to me that you should look at the actual document that your client agreed to. I could be very wrong on this thought also, but it seems to me that this type of arrangement may fall under IRC sec 1041 that deals with transfers of property incident to divorce, and because the heart of the Gillmore decision is that one spouse can't take actions to deprive the other party to division of assets to which that other party is entitled to (by refusing to retire). That's a long-winded way of saying I don't know. Sorry & good luck! Maybe someone else has experience that will clarify, and hope you will post what you find out.

-

No, can't claim the EIC now. https://www.irs.gov/businesses/small-businesses-self-employed/filing-past-due-tax-returns From the above linked IRS page:

-

The firms I worked for kept time in 6 min 10ths of an hour because some things don't take 15 minutes, and when that quarter hr was tried the time charged to clients was more than actual. I still use 6 min 10ths of an hour, and so do a few others I know of.

-

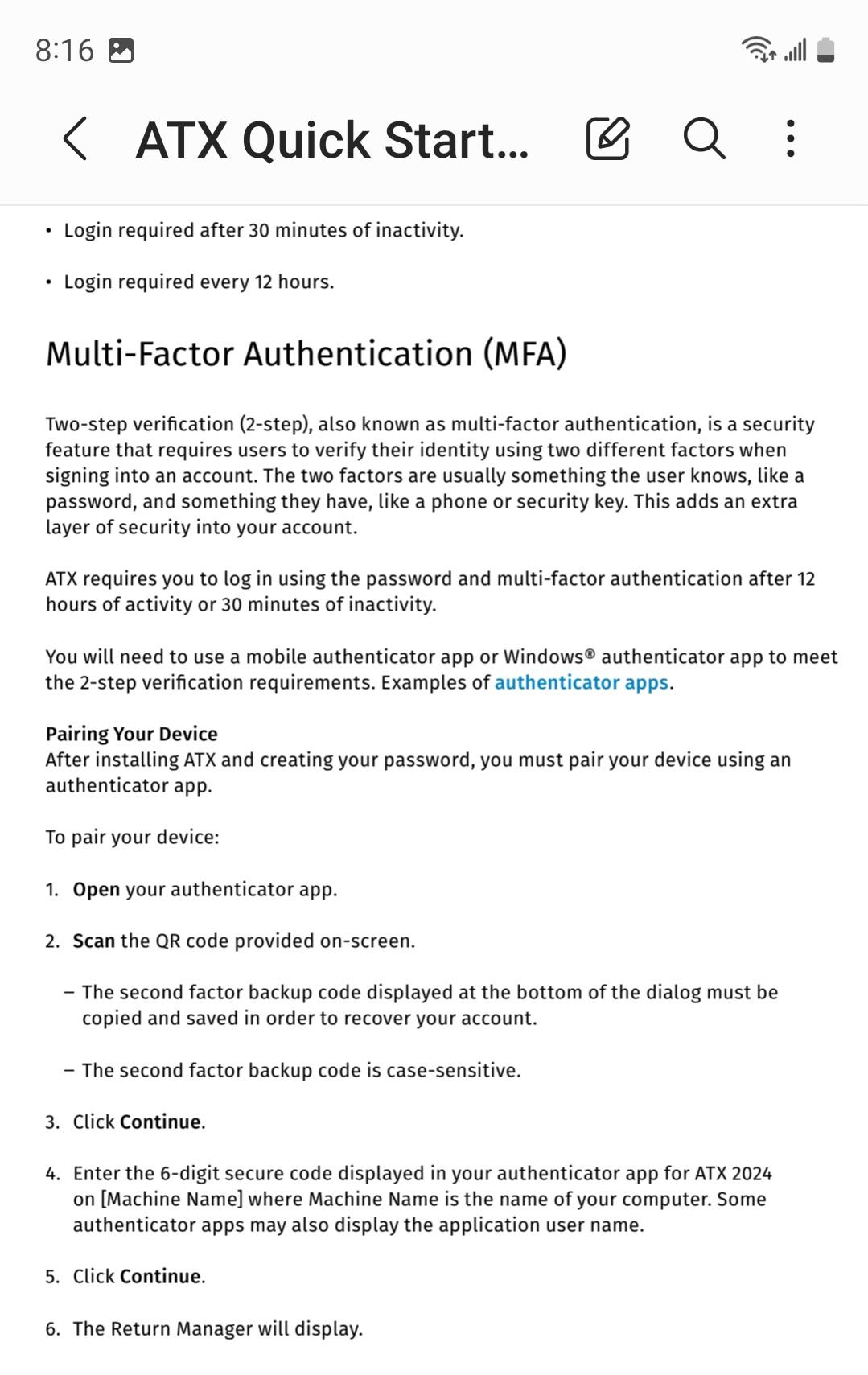

This is a screenshot from the ATX Quck Startup Guide. Note the 2 bullet points under step #2 where it says that during the pairing of the device there is a backup code at the bottom of the ATX screen that must be copied and saved that would allows user recovery. The would be used in the event the MFA device is lost or no longer working.

-

Tom, thanks for clarifying. Maybe I should think about retiring.

-

Why me? Now? Multi-state psychologist issue

jklcpa replied to Margaret CPA in OH's topic in General Chat

Margaret, I'm sorry to have completely missed the point that you are asking about travel related expenses when being away from the main tax home. With the indefinite time of duration, I'd say this doesn't qualify to take those deductions for the OH expenses. -

I'm confused by this and Tom's answers about the W2 proration as well. I don't do CA returns, but I thought CA was a stickler for any out of state person working remotely for a CA based business doing business in CA to tax all of those wages regardless of where the employee was located. Has something changed with that? My original answer about the K-1 income was going to be that all income on the K-1 is taxable to each of the 3 shareholders as CA source income and taxable there with those people claiming a credit on their OK resident personal returns for taxes paid to CA.

-

Why me? Now? Multi-state psychologist issue

jklcpa replied to Margaret CPA in OH's topic in General Chat

In general, this would fall under the office-in-home rules, if she qualifies for that. Remember that in addition to being an area of exclusive use, it also has to be regularly used for the business, so that may knock her out for this deduction since your original post said it was rather sporadic or of limited use. IF she did qualify for the OIH, this would be a further proration of her share of the net expenses after reimbursement from the other party: rent, renter's insurance, utilities, internet, telephone, etc. Considering all of that, again IF she qualifies, she may find that the business % of her share of the expenses doesn't amount to much tax savings or worth the hassle, but that is for you to discuss and advise. -

Is the "contemporaneous" receipt still around?

jklcpa replied to Corduroy Frog's topic in General Chat

IRC sec 170(f)(8)(C): scroll down linked page to 8C where it says: -

The first thing is that the anchor that presented this did not tell viewers that IRS would be sending payments automatically, and I really don't want to have to waste time on questions and conversations again to prove that they already got it and aren't entitled to more!