jklcpa

-

Posts

7,103 -

Joined

-

Days Won

396

Everything posted by jklcpa

-

Sometimes though, it is a holdup on the states' side of the testing, not the software vendor.

-

Is this the first form 943 for this farmer? Maybe this to consider from the instructions:

-

re: the zip code, I realize that the official pronouncements indicate the county. I only mentioned the zip code because the IRS used that to include that ever so helpful insert for you to consider the disaster relief for your late filing. Without indicating why you filed late, the IRS' system just saw a late return but based on your zip code, said you might be able to use the disaster relief as the reason. Your post trigger the memory of paper-filed returns with notations at the top such as "filed pursuant to blah, blah" and was the reason I asked. My return is usually one of the earlier ones filed because I use it as the test.

-

I've used efilemyforms.com for a few years with ease.

-

This morning 9am eastern https://www.irs.gov/e-file-providers/modernized-e-file-mef-status

-

Yes, it was supposed to open at 9am ET today.

-

True. I agree. One thing I'd wish for is if we could get rid of the program timing out and requiring us to log in again.

-

More convenient and maybe OK for a desktop, but isn't it somewhat less secure to have it on the same machine if that machine is compromised. I also see this setup as less secure on a laptop that travels with the preparer. If the laptop is lost or stolen, the MFA is there on the same machine as the tax software, or whatever program or internet site the MFA is protecting.

-

I think IRS goes by zip code and would be the reason you received that insert with the notice. I am curious though, did you indicate the disaster area and reason for the late filing and then IRS ignored that? If using Drake, that would be entered on the MISC screen.

-

Here are 2 articles worth reading: https://www.thetaxadviser.com/issues/2022/oct/10-good-reasons-why-llcs-should-not-elect-s-corporations.html https://www.hinckleyallen.com/publications/converting-an-llc-to-an-s-corporation-a-mistake-waiting-to-happen/

-

Not enough information to answer. Is it a vacation rental used by owner?

-

Sometimes I'm lucky with searches, I guess.

-

Here's the whole page of IRS newsroom announcements by year, if that isn't the one: https://www.irs.gov/newsroom/tax-relief-in-disaster-situations. Also, here's a link to Rev Proc 2018-58 . link to it. Look in Sec 8, item 11 where it says this:

-

Maybe, but it may depend specifically on which disaster and what exactly was extended. The IRS publishes guidance for each specific disaster that has all the details. I skimmed through and found one for FL related to Hurricanes Milton and then Debbie that may be the one you are asking about. IF that is the issue, then the answer appears to be yes if your client had a valid extension until 10/15/24. It was the 12th bullet point down listed under 2024 that encompasses all of FL relief, and there were other IRs for each of the specific disasters below it. Anyway, the one linked does "stack" the relief, as you put it. https://www.irs.gov/newsroom/irs-announces-tax-relief-for-victims-of-milton-various-deadlines-postponed-to-may-1-2025-in-all-of-florida In the 4th paragraph under "Affected Taxpayers" it refers back to Rev Proc 2018-58 for the additional deadlines for payments to be extended and IRA contribs is one of them.

-

Paste it into some sort of text document via Word or Notepad and save that document. Probably a good idea to save it on the computer and print it too. The code doesn't work anywhere now and would only be used as part of the recovery process if your phone is lost/stolen/broken.

-

This is beyond me, and I'm not thinking clearly ATM anyway. Even if I could though, this needs to be incorporated in their overall estate plans, so I'd be sending them to an attorney that specializes in tax and estate planning.

-

Yes, that would be it.

-

Watch the following ATX support video starting at 4:25 minute mark for how to reset the pairing. You will need your activation code to do this. You will have to go through pairing the device again and will show that recovery code at that time. https://support.cch.com/oss/sfs/video/U7mpfMUm17s

-

Probably puts it in the computer's clipboard for use in pasting somewhere else, as in copy and paste.

-

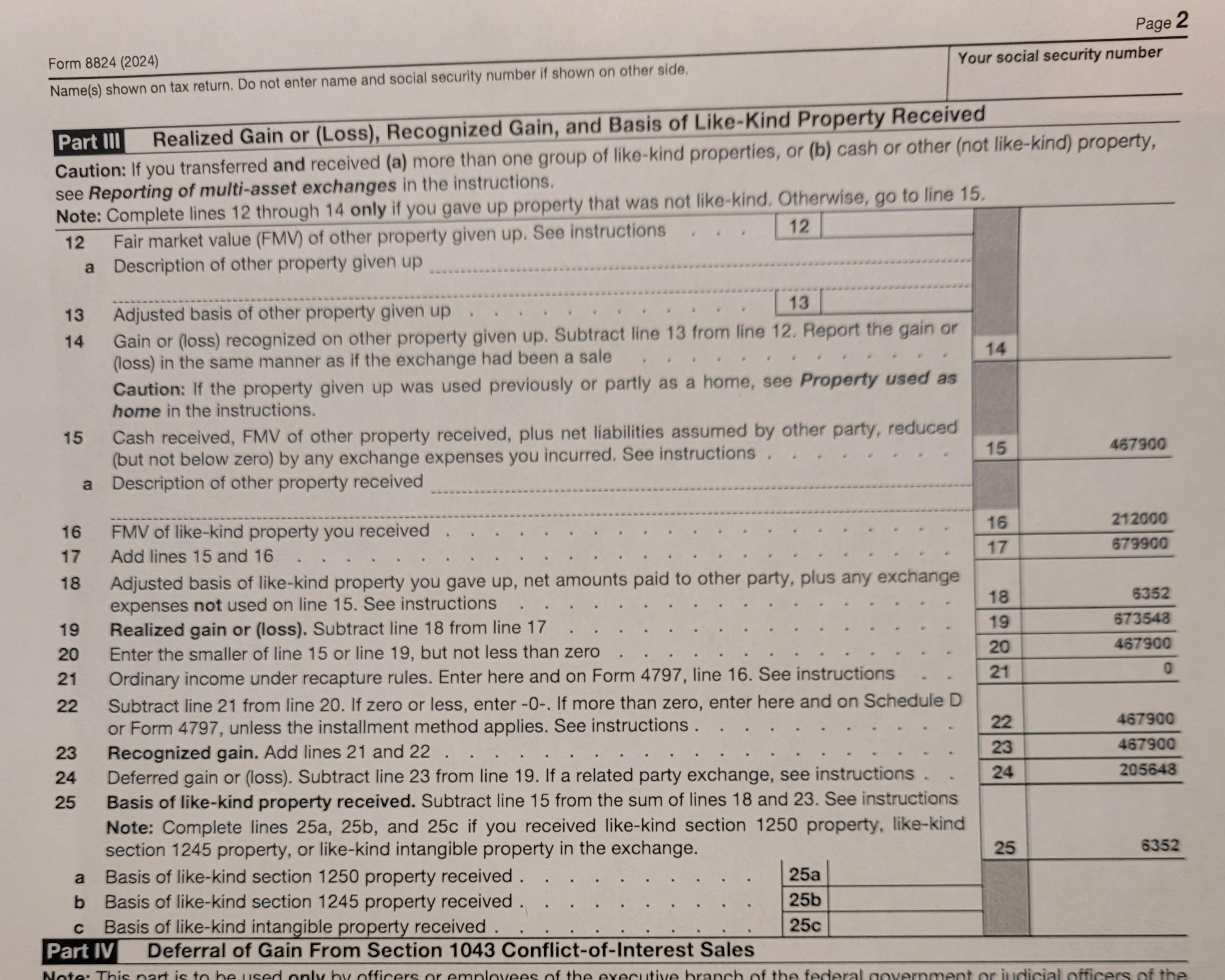

Sorry if that pdf isn't working. It has been an ongoing issue since the upgrade. Here's a photo that may work

-

Margaret, that 8824 definitely has problems and shouldn't be relied on, and I think you are going to have to rework the numbers to arrive at the proper deferral. In a general and simplified discussion, the deferred gain should be the difference between recognized gain and the realized gain. Maybe think of it as a reconciling exercise where that deferral reduces the basis of the new property back down to that of the old (new property as if purchased outright minus the deferred gain = basis of the new). It's not unlike the very old personal residence rules where the basis was reduced when gain was deferred. In a very simplified example, I've created an 8824 with your facts. I'm not sure where some of the former preparer's figures come from, and I don't have the selling expenses or other costs that you mentioned, so below is a very basic 8824 with your fact pattern to use as an example. You'll see that the deferral on line 24 is the difference between the recognized and realized gains (line 19 minus 23), and that amount is the exact reduction applied against the new property, and that brings you back to the basis of the old. Also, keep in mind that "cash received" on line 15 isn't the cash received at settlement of selling the old; it is the cash that the seller didn't reinvest, so my starting point was $679,900 - 212,000 reinvested. The use of $212K accounts for the $5K of fees. Maybe this will help you sort this out. And if I'm all wrong here, Dan will straighten me out. 8824.pdf

-

@Lion EA Is the client trying to use Direct Pay as a guest where it doesn't require log in? You said the client was able to log in to his IRS account and check his address. Did he try to make the payment while logged in there? Sorry if I'm missing something there. I have an EFTPS account for this so haven't personally gone through all of those steps on that page.

-

I know, it sounded ridiculous to me too but was passing on what worked for one person.

-

One suggestion I saw from someone that was also having difficulty, specifically with the address, was to type it in all caps. As you already suggested, he should try again on another day. The only other way other than what you've already mentioned is to pay by same-day wire transfer that the TP's bank initiates. Scroll to the bottom of this IRS payments page and you should see a link to another page. That next page has a link to a payment information worksheet in pdf form for the TP or business to fill out and present to the bank. Hope it isn't an identity theft issue. Sorry he is having troubles.

-

I had a thought on the land. Was this a condo where no amount was assigned to land? Other than that thought, concerning future sale and gain: as you know, the premise of the 1031 is that the basis of the new carries over from the old property given up so that any gain is deferred to the future, so -0- basis would be possible if every bit of the property given up has been depreciated, but there is still my question about the land. It is possible that the full amount of proceeds of a sale in future, net of exps of sale, would be the amount of gain from that future sale if the property truly has -0- basis. Then again, the TP will have additional basis for any capitalized costs incurred after the 1031 exchange occurred.