jklcpa

-

Posts

7,105 -

Joined

-

Days Won

396

Everything posted by jklcpa

-

A snippet from this article from Wed April 27th:

-

I agree with you and Yardley that there is no downside to this provider supplying the identifying number, and it is up to the taxpayer to determine if he/she meets all of the other rules for claiming the credit. You are correct that pub 503 specifically mentions that soccer camp IS an allowable expense, but then goes on in the examples to show that camps including recreational activities are allowed IF the taxpayer and dependent otherwise meet all the other tests of the credit including the dependency and work-related tests by using the phrase "may be eligible" not "is eligible." If it helps, dependent care credit is covered in IRC sec 21, and the definition of employment-related expenses is at sec 21(b)(2), and then the special rules at sec 21(e)(9) and (10) covers identifying information of the service provider, but it doesn't specifically mention the W-10 but only that the taxpayer must show due diligence in his/her attempt to include all of the required information on the return pertaining to the service provider. https://www.law.cornell.edu/uscode/text/26/21 I think my software would not allow e-filing if the EIN or other required information is missing but would have to test it to be sure. YMMV.

-

Make sure to mention that in your convo with Drake's team.

-

Hi Herbert and welcome to the forum. Did you have a question for us? I see you own a tax practice in GA. Are you a current ATX user or looking to switch to it and want a demo?

-

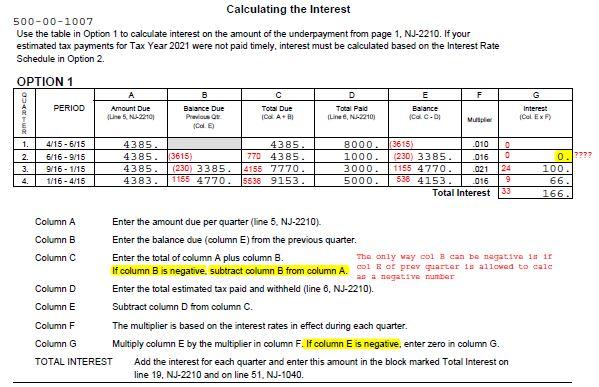

@tax1111, Below is what I created using the practice return. Drake's calcs are in black and my corrections are in red. You may have to supply something like this to Drake's programmers if you have any hope of having them correct this. I did post this same thing over in Drake's official forum for state issues, and I tagged Merry so that she may possibly intervene on your behalf and direct this to the NJ programmers. Also, if any users of other software (ATX, Proseries) could confirm if your program is generating this schedule that allows the negatives in columns B & E in support of this, that would be great.

-

Looking at the schedule that Drake produced from my hypothetical input using a practice return, it is clear to me that there are errors in Drake's output. My schedule had a positive amount (incorrectly, but ignoring that fact) in col e for the 2nd qtr but didn't multiply that out in any way and reported a zero in col G for that quarter. You are correct, it makes no sense!

-

I see what you mean about the Option 1 worksheet, because I input enough in a practice return to force the NJ2210, and I also tried it in 2019 with the same issue you are having. I don't see any way to override this calculation or line 51 of the NJ-1040 in Drake, and it doesn't seem that this is a NJ error but IS a Drake error. You have only the options to print or suppress the NJ2210. I'm sorry. I think you should call in to Drake's support if you haven't done so already. From the instructions below that worksheet, Col E is clearly intended that it can be a negative (based on instructions for Col G that says "if Col E is negative") and Col B is also allowed to be negative (based on Col C instructions that says "if Col B is negative...."). ETA - I also posted this in response to your same question over in the Drake forum so that others may see what answer you've already been given and won't be starting over with saying the same thing or may refute my idea. I'd also like to see the resolution to this issue because I have some clients that work in NJ and may run into this in future.

-

What is in 1st qtr column A, line 13? Is that not carrying over to col B, line 7 and so forth? Was the 1st qtr estimate paid timely on or prior to 4/15/21, and is that entered correctly in the software? Is this ATX or other software?

-

NT, but definitely IRS - specifically, IRS-CI, and the good they can do

jklcpa replied to Catherine's topic in General Chat

Wow, interesting read. Thanks for sharing this. -

Yes, I noticed this too. The worst was the when all the technical people assigned to the accounting program were helping with tax questions even though I'd called the phone # supposedly dedicated to the accounting support. Then the person proceeded to chastise me for expecting accounting support help saying "you know this is tax season, right?" and my answer of "yes, and you know this is 3 days before the Jan 31st filing deadline for all the information returns, payroll returns, and W-2s that I should be using your program for but am unable to do so." You know when I got the call back with help for their program that was stuck in an update loop and wouldn't load - it may have been around Feb 3rd after I'd used an online vendor for my filings, filed W-2s directly on SSA's site, and hand-prepared the 941s and 940s and mailed them in. At that point on Feb 3rd, I would never need to use the program again, ever. What a complete waste of time and money for that less-than-useless program. Tax support was fairly useless also.

-

To answer Christian so that he may make sense of how this should be reported: Christian, because your client used MACRS SL deprec, you are correct that there is no recapture of excess depreciation like happens with sec 1245 tangible property. That would be where that portion of gain is split out and the recapture portion is taxed at ordinary rates. That is NOT what is happening in your case. What is happening - when real property is sold (sec 1250 property) that has been depreciated, that portion has the potential to be what is called "unrecaptured sec 1250 gain" and that portion of the gain equal to the depreciation taken is carved out and can be taxed at a special rate up to a maximum of 25%, and that rate depends on the taxpayer's tax bracket. Obviously with that carve out, it may be possible that the unrecaptured portion exceeds the total gain, but basically, carve it out and split the gain into its components that are taxed at different rates. As cap gains, both of these portions of gain are able to be offset by cap losses, again obviously within the cap gain/loss rules and mechanics of Sch D. Here is an example that may help: Real property purchased $150K, accum deprec $30K, adjusted basis $120K Sold for $185K, generates an overall gain of $65K Unrecaptured 1250 gain is $30K (the amount of depreciation) and is subject to the higher cap gain rate with max of 25%, and the remaining gain of $35K would use regular cap gain rate.

-

You may want to have the client pay the 1Q'22 estimate now. Yes, it will be late, but will help minimize any 2210 penalty, if any, by paying that as close to the due date as is possible. Client's options now for paying the 2nd, 3rd & 4th estimates are by check, direct pay, or EFTPS.

-

So do I, and the current filing should update banking info in the states' and federal systems.

-

Catherine said this started as a state issue though.

-

Never seen it either. How did that happen?

-

It's 41 yrs for me and not thinking of retirement yet either.

-

https://www.irs.gov/taxtopics/tc206 https://www.irs.gov/payments/dishonored-check-penalty Must show reasonable cause and that the taxpayer had the expectation that the payment would have been honored.

-

Use federal form 5695 if it's the 26% Federal (ITC) solar credit you are asking about. It's not at the state level.

-

I am, maybe. I spent the morning waiting at my mom's house for Comcast to come fix her cable and am going to watch a White Sox game next.

-

Next section below that in same IRM under #3

-

From IRM here: https://www.irs.gov/irm/part3/irm_03-017-278#idm140034069386688

-

I've seen that IRS will try to w/d a payment on an installment agreement on the next scheduled date, but that is not what you asked. Not sure if it would try to resubmit in the case you described, but pretty sure it wouldn't take a different amount than was authorized. The IRS may eventually send Letter 608C Dishonored Check Penalty, but at this point I'm not even sure if this letter is one that the IRS included not sending in its recent effort to get caught up on the backlog and had recently stopped its computers from sending out repeated letters. The way to know for sure is for the client to verify with his/her bank. Sorry, not much help.